You check your banking app and suddenly notice a charge you don’t recognize.

Panic kicks in. Was your card hacked? Did you accidentally subscribe to something weird at 2 AM? Or did a company simply bill you twice?

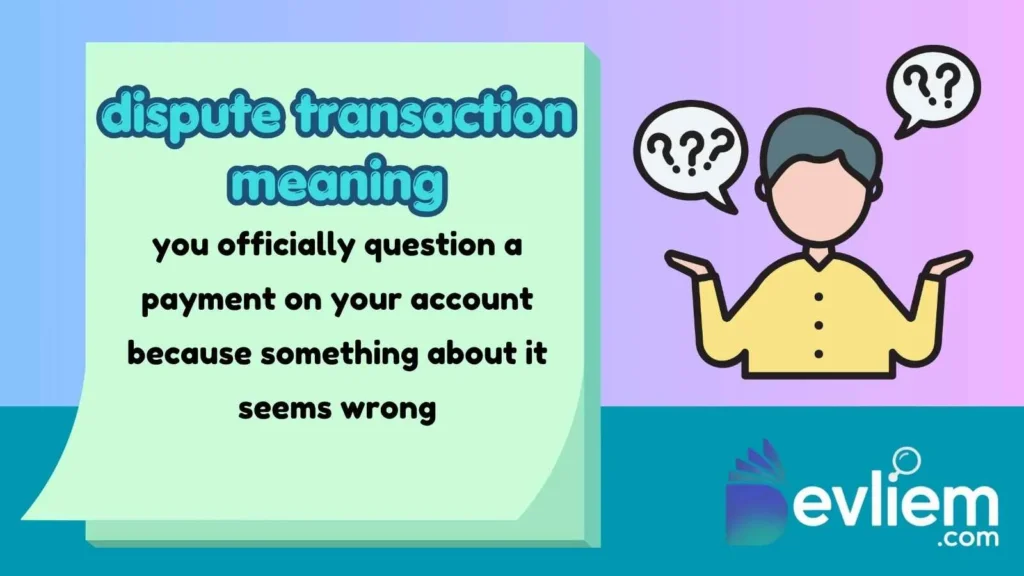

That’s where understanding dispute transaction meaning becomes incredibly important.

In today’s digital world, online payments happen in seconds. But mistakes, scams, duplicate charges, and unauthorized purchases happen just as fast.

Knowing how transaction disputes work can help protect your money, avoid fraud, and save hours of stress with your bank.

This guide breaks everything down in plain English. You’ll learn what a disputed transaction actually means, why people file disputes, how banks investigate them, common mistakes to avoid, and real world examples that make the process easy to understand.

Updated for 2026, this guide also covers how disputes work across credit cards, debit cards, PayPal, mobile wallets, and modern banking apps.

What Does “Dispute Transaction” Mean?

A dispute transaction happens when a customer challenges a payment or charge they believe is incorrect, unauthorized, fraudulent, or unfair.

This usually involves contacting the bank, credit card company, or payment provider and asking them to investigate the transaction.

Quick Answer:

A dispute transaction means , suspicious, or unauthorized.

The phrase became more common as online shopping, digital banking, and mobile payments exploded in popularity during the 2010s and 2020s. Before that, disputes mostly involved credit card fraud or billing errors over the phone.

Today, transaction disputes happen on:

- Credit cards

- Debit cards

- Banking apps

- PayPal

- Apple Pay

- Google Pay

- Online shopping platforms

Pronunciation Guide

Dispute transaction is pronounced:

dis-PYOOT tran-ZAK-shun

How to Use “Dispute Transaction” Correctly in Banking & Finance

Unlike internet slang, this term is mostly used in financial and banking situations.

People often use it when:

- Talking to customer support

- Reporting fraud

- Requesting charge investigations

- Explaining payment issues

- Filing chargebacks

Common Usage Examples

- “I disputed the transaction because I never made that purchase.”

- “My bank opened a dispute transaction investigation.”

- “The payment is currently under dispute.”

- “You can dispute unauthorized charges within 60 days.”

Where You’ll See the Phrase

Banking Apps

Most apps now have a “Dispute Transaction” button directly inside payment history.

Credit Card Statements

Banks often label disputed charges as:

- Pending dispute

- Transaction under review

- Chargeback initiated

Customer Support Chats

Agents may say:

- “Would you like to dispute this transaction?”

- “Please upload proof for the disputed payment.”

When NOT to Use It

Avoid using “dispute transaction” casually outside finance or payment discussions. It’s a formal banking term, not slang.

For example:

❌ “I disputed the pizza transaction because it tasted bad.”

✅ “I requested a refund from the restaurant.”

How Transaction Disputes Actually Work

A lot of people assume disputing a charge instantly returns their money forever. Not quite.

Here’s the normal process.

Step 1: Customer Notices a Problem

The issue might be:

- Fraud

- Duplicate billing

- Wrong amount charged

- Subscription renewal surprise

- Product never delivered

Step 2: Customer Files a Dispute

This usually happens through:

- Banking app

- Phone support

- Online banking portal

Banks often ask for:

- Transaction date

- Merchant name

- Screenshots

- Receipts

- Evidence of fraud

Step 3: Temporary Credit May Be Issued

Some banks give provisional refunds while they investigate.

This is not a guaranteed permanent refund.

Step 4: Investigation Begins

The bank contacts:

- Merchant

- Payment network

- Card issuer

They review evidence from both sides.

Step 5: Final Decision

Possible outcomes:

- Customer wins dispute

- Merchant wins dispute

- Partial refund issued

- Claim denied

Real Conversation Examples Using “Dispute Transaction”

Example 1: Unauthorized Purchase

Context: Banking Fraud

Alex: “Did you buy something from Tokyo Electronics?”

Sam: “Nope. I already disputed the transaction with my bank.”

What It Conveys

Sam believes the charge was fraudulent and wants the bank to investigate.

Example 2: Duplicate Charge

Context: Restaurant Payment

Emma: “Why did they charge me twice for dinner?”

Lily: “You should dispute the transaction if they don’t refund it.”

Emotional Meaning

This suggests frustration but also a practical solution.

Example 3: Online Shopping Scam

Context: E-commerce

Jake: “The website disappeared after taking my money.”

Ryan: “Call your credit card company and dispute the transaction immediately.”

Emotional Meaning

Urgency and caution.

Example 4: Subscription Billing

Context: Streaming Service

Nina: “I canceled months ago but they still charged me.”

Chris: “That’s definitely worth disputing.”

Emotional Meaning

Annoyance over recurring charges.

Example 5: Family Discussion

Context: Parent Helping Teen

Mom: “Did you buy game coins again?”

Teen: “No! Someone hacked my account.”

Mom: “Okay, we’ll dispute the transaction tomorrow.”

Emotional Meaning

Concern mixed with problem-solving.

Common Reasons People Dispute Transactions

1. Unauthorized Charges

This is the biggest reason.

Examples include:

- Stolen card usage

- Hacked accounts

- Identity theft

- Suspicious online purchases

2. Duplicate Payments

Sometimes systems glitch and process payments twice.

Very common in:

- Restaurants

- Fuel stations

- Online checkout errors

3. Product Never Arrived

People dispute charges when:

- Items never ship

- Sellers disappear

- Tracking numbers are fake

4. Wrong Amount Charged

Maybe you agreed to pay $20 but got charged $200 instead.

That’s a valid dispute reason.

5. Subscription Traps

Some services quietly renew memberships after free trials.

Banks receive millions of disputes related to forgotten subscriptions every year.

Common Mistakes & Misunderstandings

Mistake 1: Filing a Dispute Before Contacting the Merchant

Banks usually recommend contacting the seller first.

Sometimes the issue is just:

- Slow shipping

- Billing delay

- Human error

Jumping straight to disputes can slow things down.

Mistake 2: Confusing Refunds With Disputes

These are different.

Refund

You ask the business directly.

Dispute

Your bank investigates the charge.

People mix them up constantly.

Mistake 3: Waiting Too Long

Most banks have strict deadlines.

Many card providers require disputes within:

- 30 days

- 60 days

- 120 days

Waiting too long can weaken your case.

“Dispute Transaction” Across Different Platforms & Payment Apps

Credit Cards

Credit cards usually offer the strongest protection.

That’s why fraud experts often recommend using credit cards instead of debit cards online.

Debit Cards

Debit disputes work too, but the money comes directly from your bank account.

That can make temporary cash flow stressful.

PayPal

PayPal has its own resolution center for:

- Item not received

- Unauthorized payments

- Significantly different products

Mobile Wallets

Apps like:

- Apple Pay

- Google Pay

- Samsung Wallet

still rely on your linked bank or card issuer for dispute investigations.

Buy Now Pay Later Apps

Platforms like Klarna or Afterpay may have separate dispute systems before involving banks.

This confuses many users in 2026 because the process feels less standardized.

Is Disputing a Transaction Safe?

Usually yes — if your claim is honest.

Banks expect customers to report:

- Fraud

- Scams

- Billing errors

But false disputes can cause problems.

Some people abuse chargebacks after legitimately receiving products. That’s called “friendly fraud,” and businesses fight it aggressively now.

Merchants may:

- Ban repeat abusers

- Send debts to collections

- Challenge disputes with evidence

So only dispute charges when you genuinely believe something is wrong.

Dispute Transaction Across Different Generations

Gen Z

Younger users often dispute:

- Gaming purchases

- App subscriptions

- TikTok shop orders

They expect instant app-based support.

Millennials

Millennials commonly dispute:

- Streaming subscriptions

- Travel bookings

- Online shopping charges

They’re usually comfortable using mobile banking tools.

Older Generations

Older users may prefer:

- Calling banks directly

- Visiting branches

- Speaking with human agents

Many are more cautious about online fraud.

Related Banking Terms, Slang & Alternatives

| Term | Meaning |

|---|---|

| Chargeback | Forced payment reversal through the bank |

| Refund | Merchant voluntarily returns money |

| Unauthorized Transaction | Payment made without permission |

| Fraud Alert | Warning placed on suspicious account activity |

| Pending Transaction | Payment not fully processed yet |

| Billing Error | Incorrect amount or duplicate charge |

| Scam Charge | Fraudulent payment from deception |

| Card Verification | Security check for suspicious activity |

| Account Freeze | Temporary restriction on account access |

| Payment Reversal | Transaction canceled or reversed |

Related Search Terms

- Learn more about “chargeback meaning”

- Learn more about “pending transaction meaning”

- Learn more about “unauthorized payment explained”

FAQs:

What happens when you dispute a transaction?

When you dispute a transaction, your bank or payment provider investigates the charge to determine whether it was valid, fraudulent, or incorrect. During this process, you may receive a temporary refund while evidence is reviewed.

Can a bank deny a transaction dispute?

Yes. Banks can deny disputes if there isn’t enough evidence, if deadlines are missed, or if the merchant proves the charge was legitimate.

How long do disputed transactions take?

Most disputes take between 30 and 90 days. Simple cases may resolve faster, while fraud investigations or international transactions can take longer.

Do merchants get notified about disputes?

Absolutely. Merchants are contacted during the investigation and can submit receipts, tracking numbers, contracts, or communication records to defend the charge.

Can you dispute debit card transactions?

Yes. Debit card transactions can be disputed, especially for fraud or billing errors. However, protections may differ compared to credit cards.

What is a temporary credit in a dispute?

A temporary credit is a provisional refund issued by the bank while the dispute investigation is ongoing. The bank can remove it later if the dispute is denied.

Is disputing a transaction bad?

No — not when done honestly. Disputes exist to protect consumers from fraud, scams, and incorrect billing practices.

Conclusion:

Understanding dispute transaction meaning is more important than ever in a world filled with instant payments, online shopping, subscriptions, and digital scams.

A disputed transaction simply means you’re formally questioning a charge because something about it seems wrong. Sometimes it’s fraud.

Sometimes it’s a billing mistake. And sometimes it’s just a confusing subscription renewal that slipped under the radar.

The key is acting quickly, keeping records, and knowing the difference between a refund and a real bank dispute.

Next time you spot a suspicious charge, you’ll know exactly what to do and what not to panic about.

Got another confusing banking term you want explained? Drop it in the comments or explore more modern finance and internet terminology guides below.

Hi, I’m Emily Taylor, the voice behind Devliem.com, where meanings aren’t just explained, they’re made easy to understand.

I’ve always been fascinated by words, the way they change, evolve, and sometimes confuse us more than they should. That curiosity turned into a mission: to break down complex meanings, trending slang, and everyday expressions into something clear, simple, and actually useful.